当前位置:网站首页>Chapter IV intangible assets

Chapter IV intangible assets

2022-04-23 07:57:00 【Willie Y】

Chapter four Intangible assets

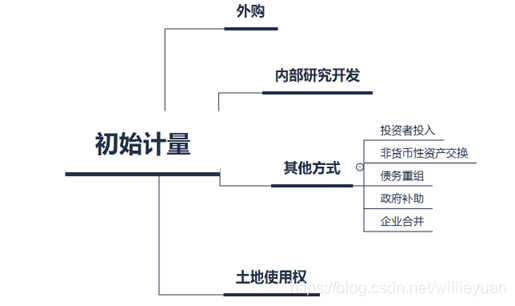

One 、 Recognition and initial measurement of intangible assets

1、 Definition and characteristics of intangible assets

features :

- Resources owned or controlled by the enterprise and can bring economic benefits to it

- No physical form

- have identifiable sex ( Goodwill is not identifiable , Not intangible assets )

- Non monetary assets

Content of intangible assets : patent right 、 Non patented technology 、 Trademark right 、 Copyright 、 The concession 、 land use right

2、 Initial measurement of intangible assets

Measured at actual cost , That is to obtain intangible assets and All expenses incurred in bringing it to its intended purpose , Cost as intangible assets .

(1)、 Outsourcing :

A、 Entry value = Purchase price + Related taxes + Other expenses directly attributable to the intended use of the asset ( Professional service fee 、 Test fee, etc )

B、 The following items are not included in the initial cost of intangible assets :

(a)、 Advertising expenses incurred to promote the introduction of new products 、 Management fees and other indirect costs

(b)、 Expenses incurred after intangible assets reach their intended use

C、 Deferred payment beyond normal credit terms ( More than a year , It has the nature of financing ), Its cost is measured at its present value

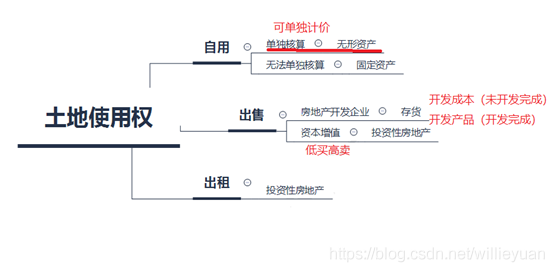

(2)、 land use right

Land use right classification :

| purpose |

features |

Category |

| Self use |

It can be calculated and priced separately |

Intangible assets |

| Cannot be accounted for separately |

Fixed assets |

|

| sell |

Real estate companies |

stock |

| Held for capital appreciation |

Investment real estate |

|

| lease |

Investment real estate |

Amortization of land use rights :

| The status of land use rights |

Included in |

| No real estate ( Own land ) |

Management cost |

| Attached property ( The ground follows the room ) |

Amortization according to the purpose of the property :

|

| The property being built |

Property costs |

Two 、 Recognition and initial measurement of internal research and development expenditure

1、 Division of research stage and development stage

It is impossible to distinguish between research stage expenditure and development stage expenditure , All R & D expenses incurred shall be expensed and included in the current profit and loss

2、 Conditions related to expenditure capitalization in the development stage

(1)、 Technically feasible

(2)、 Have the intention to complete

(3)、 Can produce economic benefits ( example : There is a market for intangible assets , There is a market for the products produced by using the intangible assets )

(4)、 There are resources to support

(5)、 Can measure reliably

3、 Accounting treatment of internal research and development

(1)、 The basic principle of

(2)、 Account processing

| First level subjects |

Secondary subjects |

Accounting treatment |

Report items |

| R & D expenditure |

Expensed expenses |

Transfer in at the end of the period “ Management cost - R & D expenses ” |

R & D expenses |

| Capitalized expenditure |

To achieve the intended purpose “ Intangible assets ” |

Development expenditure |

4、 Measurement of internal research and development

The cost of internally developing intangible assets includes The total expenditure incurred from the time when the capitalization conditions are met to the time when the intangible assets reach the intended purpose .

For the same intangible asset, before the capitalization conditions are met in the development process The expenses that have been expensed into the current profit and loss will not be adjusted .( Cannot be adjusted retroactively ).

Be careful :(a)、 At the end of the term, you need to “ R & D expenditure — Expensed expenses ” into “ Management cost ”,

(b)、 When it reaches the predetermined usable state, it will “ R & D expenditure —— Capitalized expenditure “ into “ Intangible assets ”

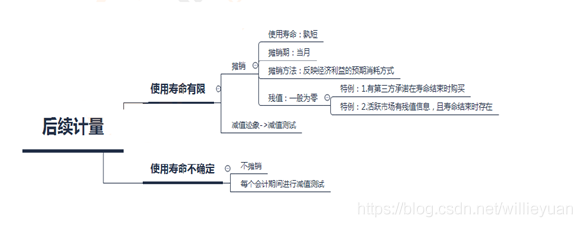

3、 ... and 、 Subsequent measurement of intangible assets

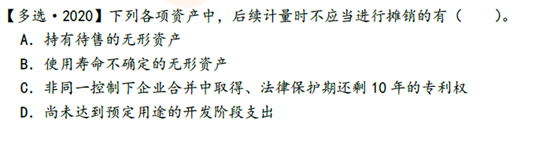

(1)、 Intangible assets Limited service life : Amortization , And the service life 、 Amortization period 、 Amortization method 、 Residual value belongs to accounting estimation . When Impairment test is required when there are signs of impairment .

(2)、 Intangible assets Uncertain service life : No amortization . but An impairment test is required for each accounting period .

(3)、 Trademark right Usually amortized to Management cost

notes : Changes in accounting estimates : Future use ( Affect the future )

Changes in accounting policies : Retroactive adjustment method ( Influence the past )

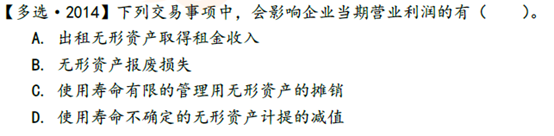

answer :ABD. Intangible assets are non current assets , and A The account of intangible assets held for sale in is Assets held for sale , It belongs to current assets ; Intangible assets with uncertain service life are not amortized , It does not belong to intangible assets when it has not reached its intended purpose , Therefore, it is not amortized .

Four 、 Disposal of intangible assets

1、 sell

The sale of intangible assets does not need to be included in the liquidation account , The sale of fixed assets needs to be included in “ Liquidation of fixed assets ” subject .

- direct sales

borrow : Bank deposits

Accumulated amortization

Provision for impairment of intangible assets

loan : Intangible assets

Taxes payable —— VAT payable ( Output tax )

Gains and losses on disposal of assets 【 Difference , Or in the debit 】

(2) According to the non current assets held for sale 、 Accounting treatment according to relevant regulations of the disposal group

2、 lease

borrow : Bank deposits

loan : Other business income

Taxes payable —— VAT payable ( Output tax )

borrow : Other business costs ( Limited service life , To be amortized )

loan : Accumulated amortization

3、 Scrap

borrow : Non operating expenses

Accumulated amortization

Provision for impairment of intangible assets

loan : Intangible assets

answer :ACD.C The amortization of management intangible assets with limited service life is included in the management expenses , Affect operating profit ;D The impairment loss of intangible assets is not included in the impairment loss of intangible assets , Affect operating profit ( Income statement I/S).

answer :ACD.

版权声明

本文为[Willie Y]所创,转载请带上原文链接,感谢

https://yzsam.com/2022/04/202204230628042373.html

边栏推荐

- linux下mysql数据库备份与恢复(全量+增量)

- SQL sorts string numbers

- Unity 获取一个文件依赖的资源

- 从零开始完整学习机器学习和深度学习,包括理论和代码实现,主要用到scikit和MXNet,还有一些实践(kaggle上的)

- Shapley Explanation Networks

- 保研准备经验贴——18届(2021年)中南计科推免到浙大工院

- C SVG path parser of xamarin version

- Internal network security attack and defense: a practical guide to penetration testing (5): analysis and defense of horizontal movement in the domain

- Simplify exporting to SVG data files and all images in SVG folder

- Understanding the Role of Individual Units in a Deep Neural Networks(了解各个卷积核在神经网络中的作用)

猜你喜欢

STO With Billing 跨公司库存转储退货

常用Markdown语法学习

Houdini流体>>粒子流体导出到unity笔记

Internal network security attack and defense: a practical guide to penetration testing (5): analysis and defense of horizontal movement in the domain

SQL sorts string numbers

Mongodb starts warning information processing

![[unity VFX] Introduction notes of VFX special effects - spark production](/img/bb/a6c637d025dfb8877e6b85e7f39d6b.png)

[unity VFX] Introduction notes of VFX special effects - spark production

CTF-MISC总结

Shapley Explanation Networks

Protobuf use

随机推荐

A programmer who works four hours a day

使用flask时代码无报错自动结束,无法保持连接,访问不了url。

Nodejs (VI) sub process operation

MySQL in window10 version does not work after setting remote access permission

SAP GUI安全性

Scrapy modifies the time in the statistics at the end of the crawler as the current system time

Index locked data cannot be written to es problem handling

Double sided shader

RGB color to hex and unit conversion

Protobuf 使用

Online Safe Trajectory Generation For Quadrotors Using Fast Marching Method and Bernstein Basis Poly

MySQL8. 0 installation / uninstallation tutorial [window10 version]

KCD_EXCEL_OLE_TO_INT_CONVERT报错SY-subrc = 2

Intranet penetration series: icmpsh of Intranet tunnel

Unity获取真实地理地图应用Terrain笔记

《内网安全攻防:渗透测试实战指南》读书笔记(八):权限维持分析及防御

Houdini > variable building roads, learning process notes

庄懂的TA笔记(零)<铺垫与学习方法>

Dropping Pixels for Adversarial Robustness

Quick sort